Wills, Trusts & Life Planning

Planning ahead gives you certainty and peace of mind. We provide clear, practical advice on wills, trusts, and life planning to help you protect your assets, provide for your loved ones, and ensure your wishes are carried out.

Planning for the future is about making informed decisions and putting the right structures in place to support you and those close to you. Whether you are considering a will, establishing or managing a trust, or planning for future decision-making, our team provides clear, practical advice tailored to your circumstances.

We work with individuals and families at all stages of life - from straightforward arrangements through to more complex family and asset structures. Our focus is on helping you protect what matters most, provide for your loved ones, and create clarity for the future.

Will Questionnaires

We offer two pathways to help you get started. Our fixed fee option is designed for couples with straightforward circumstances who require wills and enduring powers of attorney. For all other arrangements, including individuals, blended families, or those with trusts and more tailored planning requirements, we provide a bespoke service tailored to your circumstances.

Areas We Can Help With

-

Mactodd Lawyers assist with all of your or your loved ones’ estate administration needs. This includes court applications for probate of the will if necessary, or letters of administration where there is no will. We also advise and assist with international considerations to do with obtaining probate or letters of administration, such as resealing and exemplification. The value of careful estate planning and estate administration cannot be underestimated in mitigating difficult and costly issues once you or your loved one has passed away. You will find the below free guide a helpful overview on processes to complete once someone passes away, including administering and distributing the estate.

The Closing Chapter

A practical guide to help deal with the death and estate of close family or friends.

When someone close to you dies, whether family or a close friend, it’s a time of shock and dealing with the unexpected, as well as your own feelings of grief and loss.

You’re catapulted into thinking about organising a funeral, whether it will be a cremation or burial and how to organise the day, and then you also need to think about the Will and all the ramifications of dealing with the estate.

This booklet provides an overview to help you if you’re doing some preplanning, or organising a funeral of a family member or close friend.

We’ll guide you through the steps you need to take from the time of your loved one’s death through to their funeral.

Most of The Closing Chapter, however, focuses on what happens with the Will and the estate. There’s information for executors, trustees and beneficiaries as well as material about claims against an estate, dealing with small estates and what happens when there’s no Will. We’ve also covered some topics, such as asset planning, that beneficiaries of the estate may find useful.

We’ve provided a checklist of what to bring to the first appointment with the estate’s lawyer, as well as a step-by-step guide on clearing up the estate.

At the back of the booklet there’s a glossary of terms that you will hear as the necessary legal processes are worked through.

The Closing Chapter is designed for readers to ‘dip into’ and not necessarily for you to read cover-to-cover, so we have tried to ensure that each section is as complete as possible in itself. In order to do this, there is, of necessity, some repetition of material.

The death of a family member or close friend is a very emotional time. Even if the death wasn’t sudden, you have to work through grief and, often, a major change in your life. We hope this booklet helps to explain the processes and procedures around the death of a family member or close friend, gives some advice about organising a funeral and guides you through what to do in dealing with their estate. We also hope that you get some comfort from knowing there’s a guiding hand for you.

-

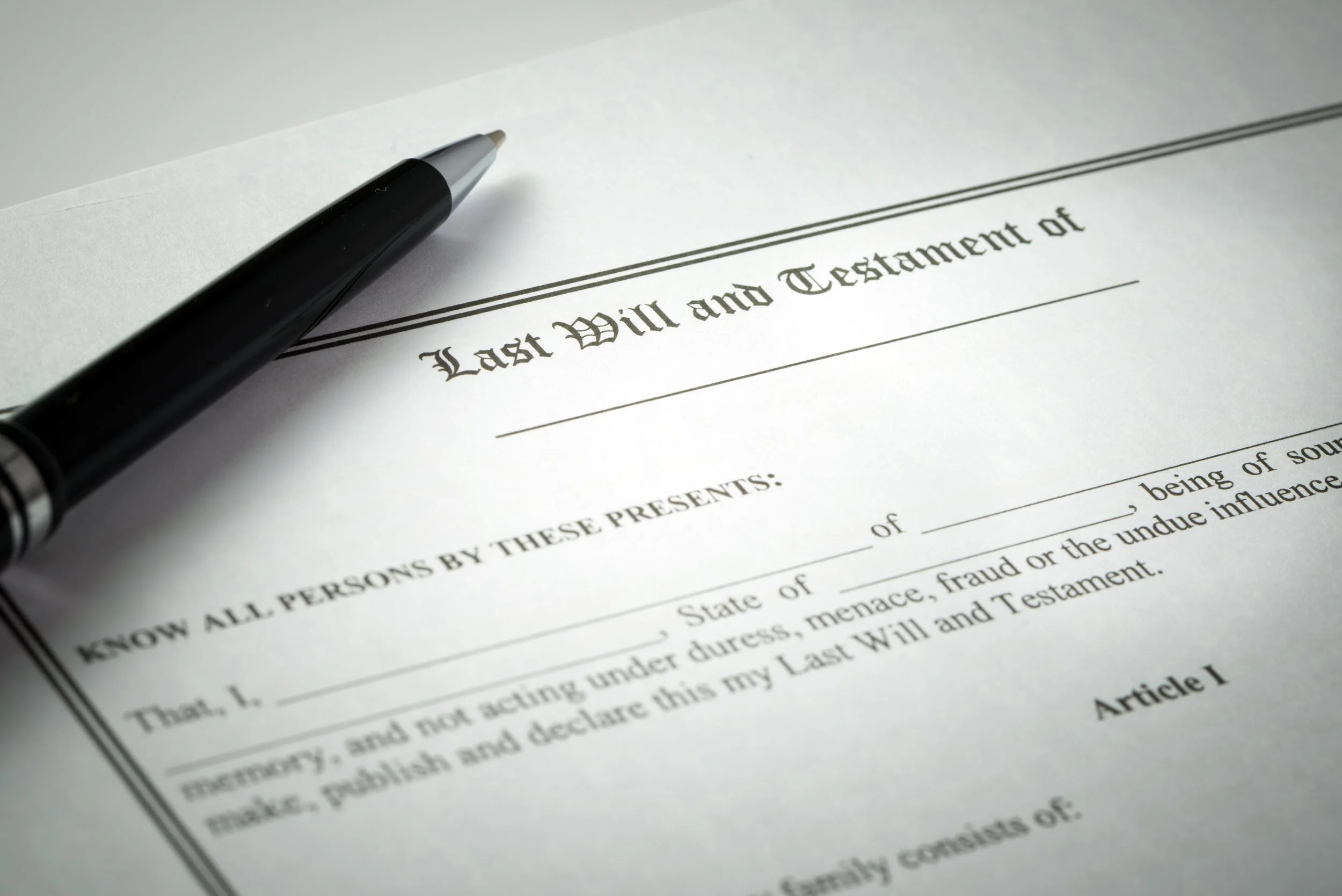

What is a Will and why do you need one?

A Will is a document that sets out how you want your affairs dealt with after you have passed away. It is legally binding, and cannot be changed after death without application to the Court.

What sort of things could you include in your Will?

You want to leave your money to your partner/spouse, your children, or to someone else

You want to leave your house to someone specific

You want to leave your jewellery to your sister

You want to leave your pets to your brother

You want to make a gift to a charity

You want to appoint your sister as guardian of your children

You want to be buried in a certain place or cremated and your ashes scattered at the top of the Remarkables

Who carries out your wishes?

In your Will you will appoint one, or more, executors to carry out your wishes. You should think carefully about who you want this to be as it is a very important and sometimes time-consuming position.

When should you update your Will?

If you change your mind about anything substantial, or your circumstances change, you should update your Will as soon as possible. A change of circumstances could include, for example, separating from your partner, having children, buying your first house, winning lotto, getting married, having a major falling out with someone you have gifted something to, or your intended guardian of your children dying. You need to consider all your family members and ensure that none are unfairly excluded.

What happens if you don’t have a Will?

If you own property worth more than $15,000 someone will need to apply to the Court to have your estate administered. Without your wishes, the law will apply to who gets how much of your estate. Generally, your partner, spouse, civil union or de facto partner will benefit first, then your children, parents, siblings and so on. If there is no-one surviving you then your assets will belong to the Crown and will be distributed according to the legislation.

Making a Will can sometimes be difficult and you need to be sure you have thought about all your options. Mactodd are here to help you with this.

-

Enduring Power of Attorney

An Enduring Power of Attorney is a legal document that gives someone you appoint the power to make decisions for you in the event you are no longer able to. The person or persons you appoint are known as your Attorney. An Attorney can make decisions about your property, finances and your personal care and welfare.

Why you should have an Enduring Power of Attorney

If you have an event or episode and you don’t have Enduring Powers of Attorney in place, your spouse/partner or wider family may need to apply to the court to obtain an order to act on your behalf. This is both an expensive and stressful process.

There are two different types of Enduring Powers of Attorney

1. Enduring Powers of Attorney for Property

Under this document, the person or persons you appoint can act on your behalf either immediately or if you lose mental capacity. That choice is yours at the time you make the attorney. We can advise you and help you with that decision.

This gives your Attorney the ability to make decisions in relation to your financial affairs. For example, they could complete an application for rest home care should you require it. They can act on your bank accounts, pay your bills and buy and sell assets including your home.

2. Enduring Powers of Attorney for Personal Care and Welfare

Under this document, the person you appoint can make decisions about your personal welfare, health and living arrangements. You can only appoint one personal care attorney at a time.

These attorneys only come into effect if you lose mental capacity as certified by a Doctor or should a Court make that finding.

Setting up your Enduring Powers of Attorney

Our Team of experienced Lawyers and Legal Executives can assist you with setting up your Enduring Powers of Attorney, advising you, and protecting your interests.

-

-

It is important to review your Trust regularly

To keep everyone updated on major changes and decisions (including your trustees, accountants… and lawyers!) trusts should be reviewed after any major changes or at least annually.

We can help you make sure that all the necessary deeds are accurate and on file, all the proper future planning actions are in place, checking the register of key events and decisions, and much more.

Some important questions you should be asking yourself are:

• Do you have a memorandum of guidance for your trust?

• Does your trust owe you money?

• Have you paid off your mortgage?

• Have your family circumstances changed?Click here for a helpful flowchart to guide you.

If you have a Family Trust and want to make sure everything is up-to-date, get in touch with our Trusts & Life Planning Team – Clark Pirie, Annabelle Alloo or Caitlin Dykes

-

THE ABOLISHMENT OF GIFT DUTY

As most readers will be aware, the Government abolished gift duty in October 2011. That abolishment effectively means that a person can gift an unlimited amount of property amongst family members at any one time without incurring Government gift duty. Previously a person could only gift $27,000.00 per annum without incurring gift duty.

Whether it is beneficial for you to gift more than $27,000.00 at any one time to your Trust will depend on your own personal circumstances and your reasons for setting up the Trust in the first instance. The matters that you will need to consider are as follows:

Your solvency and the possibility of claims against you by creditors immediately and in the future;

Whether you might be gifting relationship property which could jeopardise a future claim;

Whether you intend to apply for a residential care subsidy now or in the future;

Possible claims by creditors

If you intend to gift the total balance owing to you by the trustees of your Family Trust, you must be solvent on the date that you are making the gift. To satisfy a solvency test, you must be able to pay all debts as they fall due. If you make a gift when you are insolvent then it is possible for that gift to be reversed by a Court at any time. The effect of the Court reversing the gift will place you in a position where you could make payment of some or all of your debts.

Relationship property

Gifts to Trusts that defeat relationship property rights can be overturned by a Court. In some circumstances additional claims for financial losses might also be available to a party who has suffered a loss as a result of improper gifts. The safest course is for a trust to be formed, assets transferred to it and gifting to be completed prior to the commencement of a relationship. The transfer of assets into a Trust during the course of a relationship (this can include any forgiveness of debt), may be considered as a transfer of relationship property to the trust. In the event of a relationship breakdown, the trust might thereafter be open to a relationship property claim.

Residential Care Subsidy

When applying for a rest home subsidy, certain thresholds for ownership of assets for rest home subsidy, and thresholds for historical gifting, must not be breached. A rest home subsidy will likely be available where gifting of the amount of $27,000.00 per annum and $6,000.00 per annum during the five years immediately prior to your application for a subsidy. Any person who takes advantage of the repeal of gift duty to gift more than $27,000.00 in a 12 month period to a trust will be treated as having deprived themselves of assets. The Ministry of Social Development will add back excess gifting as an asset of the individual and on that basis the applicant may not qualify for a residential care subsidy.

Our broad recommendation is that gifting programmes should continue unchanged. In some instances, it will be beneficial for an individual to forgive and release outstanding debt provided that the solvency test can be met and there are no threatening creditors on the horizon. However, it is imperative that you discuss your specific personal circumstances with your solicitor prior to making any decisions on the forgiveness of outstanding debts.

-

Planning for retirement can require careful legal and financial planning to ensure your assets are protected, your wishes are carried out, and your future needs are provided for. Our team can assist with structuring your assets in a way that supports long-term financial security while also considering tax efficiency (in consultation with your accountant) and potential eligibility for government support, such as the Residential Care Subsidy. We provide advice on family trusts; business succession planning if you own a farm or other business; international property considerations; and other inheritance and estate planning to make sure your assets pass to the right people in the right way. We also help clients understand how relationship property laws may affect retirement planning and estate distribution. By taking a proactive approach, with early legal advice, you can reduce uncertainty, avoid unnecessary disputes, and ensure that both you and your family are well prepared for the next stages of life.

-

Asset Transfers and Protection

Protecting your assets and managing transfers effectively is an essential part of long-term financial and personal planning. In New Zealand, careful attention must be given to laws such as the Property (Relationships) Act 1976, which can affect how property and investments are treated in the event of a relationship breakdown or death; as well as to tax and gifting rules that may impact inheritance and succession planning. Our team can advise on structuring asset transfers—whether during life or as part of your estate—to safeguard wealth, minimise risk, and ensure your intentions are respected. This includes guidance on trusts, succession planning, and strategies to protect assets from potential claims, all while considering eligibility for government support, such as any Residential Care Subsidy entitlements. Where applicable we may liaise with your accountant and other experts to help formulate your optimal plan. By taking a proactive approach, you can secure your financial future, provide clarity for your loved ones, and reduce the risk of disputes or unintended consequences under New Zealand law.

-

An Advance Directive can provide a way for you to gain more control over any treatment and care you are given if you experience an episode or event that leaves you unable to decide or let others know what your preferences are at that time.

It can stipulate what treatments; drugs or other medical procedures you want to be given or not. It could state the place you would like to receive those services should you experience such an episode, for example, your home.

An Advance Directive is best achieved by way of a signed written instruction setting out wishes and what treatment you want or do not want in the event that you become unwell in the future. Whilst you don’t need a Lawyer to make an Advance Directive we can help you to ensure that your Advance Directive is respected.

An Advance Directive is not a binding legal document however your Doctor or other Medical Advisors will consider following your Directive after considering several matters.

Was the Directive made freely, in other words, no one else has influenced your decisions

When you made your Directive were you competent and well-informed to make those decisions

At the time of the event or episode does the Directive apply to those circumstances or was a different set of circumstances anticipated, or is your Directive out of date.

An Advance Directive will assist and help to ensure that your wishes are considered. If you wish to put in place a more robust plan you should consider appointing someone your Enduring Power of Attorney. That person can make decisions for you and act on your behalf should you lose mental capacity.

Still have questions?

Reach out to our team for assistance.

Our Team of Specialists

-

![]()

Caitlin Dykes

Director

-

![]()

Clarke Pirie

DIRECTOR

-

![]()

Anna Gillooly

SENIOR SOLICITOR

-

![]()

Howard Alloo

SPECIAL COUNSEL

-

![]()

Madeline Patterson

SOLICITOR

-

![]()

Annabelle Alloo

SOLICITOR

-

![]()

Boome Kim

SOLICITOR

Insights & Updates

Stay informed with our latest blog posts.